For investors building global portfolios, the challenge is rarely market access or information.

It is managing uncertainty across cycles, geographies, and asset classes. Most portfolios underperform not because markets behave unpredictably, but because decisions become reactive, fragmented, and inconsistent over time.

The core problem is not identifying the best asset or timing the market correctly, but constructing a portfolio that can withstand uncertainty, control risk, and compound sensibly over the long term.

At Paasa, Modern Portfolio Theory forms the foundation of how we think about global investing.

Table of Contents

- What Modern Portfolio Theory means

- Why it remains relevant across market cycles

- Why intuition and stock picking fail over time

- Passive vs active allocation

- Why diversification matters more than asset selection

- Most overlooked risk in investing

- How Paasa applies Modern Portfolio Theory

- Why UCITS ETFs fit into Paasa’s framework

- Why global investing looks different for Indian investors

- What Paasa does not do

What Modern Portfolio Theory means

Modern Portfolio Theory begins with an acceptance of uncertainty.

Markets are unpredictable in the short term. Prices move based on information, sentiment, liquidity, and events that cannot be forecast consistently. As a result, outcomes at the level of individual stocks, sectors, or even countries remain uncertain over any given period.

Rather than attempting to predict which asset will perform best next, Modern Portfolio Theory shifts the focus to how different assets behave together over time.

Some assets perform well during periods of growth, while others provide stability during market stress. Some rise when others fall. When combined thoughtfully, these differences allow risk to be distributed across the portfolio without necessarily sacrificing long-term return potential.

Why it remains relevant across market cycles

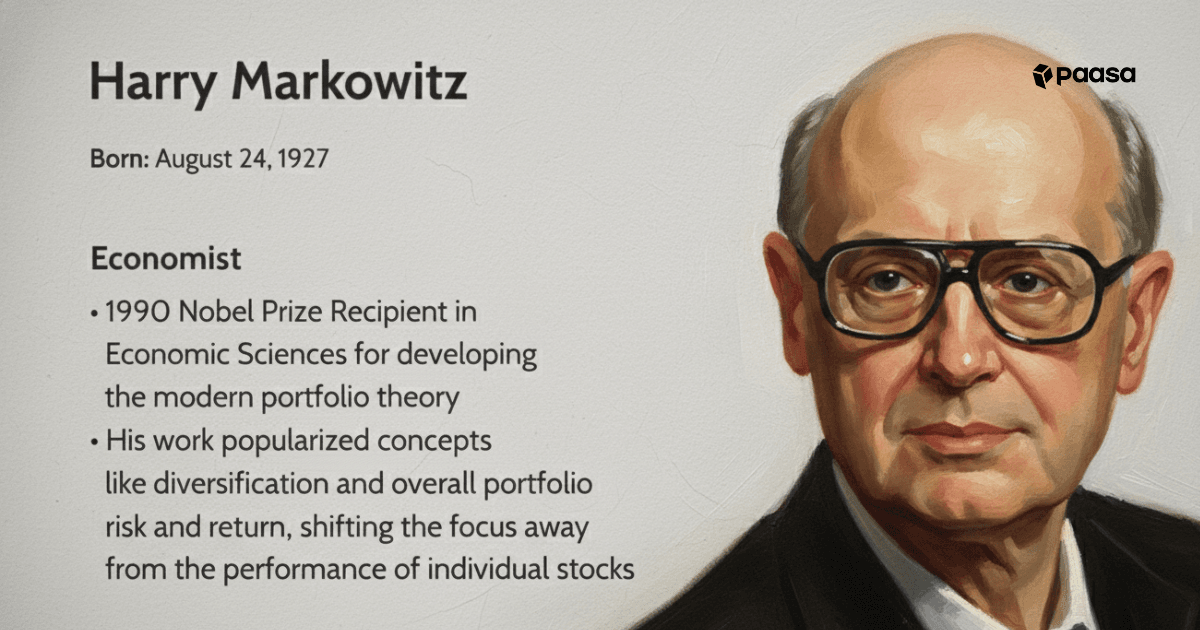

Modern Portfolio Theory was formally developed in the early 1950s by Harry Markowitz, and its core principles have been tested across more than 70 years of global market cycles.

Over the last seven decades, markets have experienced inflationary shocks, recessions, technology booms, financial crises, geopolitical conflicts, and prolonged periods of both expansion and stress. Asset classes, regions, and individual securities have repeatedly moved in and out of favour.

What has remained consistent is not which assets perform best in any given period, but how diversified portfolios behave relative to concentrated or conviction-driven approaches.

Why intuition and stock picking fail over time

As portfolios grow, intuition becomes a less reliable guide.

Concentration often feels safe because familiarity feels safe. Investors tend to allocate more capital to businesses, sectors, or geographies they know well. While this can appear prudent, it introduces hidden concentration risk that only becomes visible during periods of stress.

Stock picking also depends heavily on judgment and timing. It requires being right not once, but repeatedly, across entry points, exit decisions, and changing market conditions. Even when individual decisions are sound, outcomes remain sensitive to factors outside an investor’s control.

Over time, costs and taxes further compound this challenge. Frequent buying and selling increases transaction costs and creates taxable events, reducing net returns. This drag applies not only to individual investors, but also to professional active managers.

As a result, outcomes from stock selection and timing tend to be uneven. Periods of outperformance are often followed by extended underperformance, making long-term results difficult to predict and harder to sustain.

Passive vs Active allocation

Over long periods, most active fund managers struggle to consistently outperform the market.

While individual managers may outperform in certain years, sustaining that outperformance across cycles is difficult. Returns become increasingly dependent on timing, judgment, and repeated correct decisions, all of which are hard to maintain in uncertain and evolving markets.

Active portfolios also carry structural frictions. Frequent buying and selling increases costs and creates taxable events, leading to higher tax drag and lower net outcomes over time. Even when investment calls are reasonable, these frictions compound quietly in the background.

Modern Portfolio Theory takes a different starting point.

Rather than assuming that future winners can be reliably identified, MPT focuses on how portfolios behave across cycles. It emphasises diversification, risk distribution, and disciplined allocation over prediction and discretion.

Passive allocation aligns naturally with this framework.

Instead of attempting to beat the market, passive strategies are designed to capture broad market returns efficiently. By tracking indices through transparent, rules-based structures, passive portfolios reflect the core principles of Modern Portfolio Theory in practice.

This difference in philosophy leads to very different portfolio behaviour over time.

Passive | Active |

Tracks a broad market index | Attempts to outperform the index |

Transparent, rules-based allocation | Dependent on manager decisions and forecasts |

Lower costs with fewer fee layers | Higher fees reduce net returns over time |

Benchmark-aligned performance over long periods | Performance can vary widely year to year |

No reliance on timing or prediction | Requires correct market timing and stock selection |

Historically outperforms most active funds over 5–10 year periods | Majority underperform benchmarks after fees |

Lower tax drag, as rebalancing happens within the ETF | Higher tax drag from frequent trades and realised gains |

Why diversification matters more than asset selection

Diversification is not about owning many assets. It is about owning assets that behave differently across market environments.

A portfolio can hold multiple securities and still be exposed to the same underlying risks.

What matters is correlation.

Assets respond differently to economic growth, inflation, interest rates, and market stress. Some perform well during expansion, while others provide stability during drawdowns. When assets with different behaviours are combined, portfolio risk becomes more balanced and outcomes more resilient.

This becomes especially relevant in periods like today.

As of the end of 2025, global equity markets are trading at elevated levels after a strong multi-year run. While long-term equity exposure remains essential, portfolios that are entirely equity-driven become more sensitive to drawdowns and valuation-driven corrections.

In such environments, exposure to assets like global gold and silver can play a stabilising role. These assets do not rely on corporate earnings or economic growth in the same way equities do, and historically have behaved differently during periods of market stress, inflation uncertainty, or geopolitical risk.

In practice, diversification is less about smoothing volatility and more about managing drawdowns and regret. It allows portfolios to compound over time without relying on any single asset, market, or view being consistently correct.

This principle sits at the core of Modern Portfolio Theory and is central to how long-term portfolios are constructed at Paasa.

Most overlooked risk in investing

One of the most overlooked risks in investing is not market volatility. It is investor behaviour.

Modern Portfolio Theory recognises that even well-designed portfolios can fail if decisions are driven by emotion rather than structures like,

- Panic selling during drawdowns

- Chasing recent winners

- Overconfidence during strong markets

- Inaction during portfolio drift

These behaviours are not irrational. They are human. But they are costly and Modern Portfolio Theory addresses this risk with:

- Rules: Asset allocation ranges are defined in advance, reducing the need for ad-hoc decisions during market stress.

- Rebalancing: Portfolios are periodically rebalanced, trimming assets that have run up and reallocating to those that have lagged, even when it feels uncomfortable.

- Diversification: When different assets behave differently, portfolios experience fewer extreme swings, making them easier to hold through uncertainty.

- Process: By focusing on portfolio structure rather than individual ideas, investors are less tempted to act on short-term views.

Example

- In extended equity rallies, portfolios naturally drift toward higher equity weights as stocks outperform.

- Without rebalancing, this increases downside risk precisely when valuations are elevated.

- A rules-based framework systematically brings the portfolio back to its intended risk level, even when markets feel strong.

The goal is not to predict when markets will turn. It is to prevent portfolios from becoming fragile when confidence is highest.

How Paasa applies Modern Portfolio Theory

Our implementation focuses on structure, discipline, and risk control rather than forecasts or short-term views.

Strategic asset allocation as the starting point

Portfolio construction begins with asset allocation, not security selection.

- Exposure is spread across global equities, bonds, and precious metals to balance growth and stability.

- Allocations are designed to reflect long-term objectives and risk tolerance, not current market sentiment.

- No single asset class is relied upon to drive outcomes across all market environments.

This ensures that portfolios are not dependent on one geography, one cycle, or one economic outcome.

1) Passive ETFs as core building blocks

Paasa uses passive ETFs as the foundation of portfolio construction.

- ETFs provide broad, transparent exposure to markets and asset classes.

- They minimise costs, turnover, and unnecessary complexity.

- Returns closely reflect underlying market performance rather than manager discretion.

2) Rules-based rebalancing, not reactive decisions

Market movements naturally cause portfolios to drift over time. Paasa addresses this through rules-based rebalancing.

- Asset allocations are reviewed at defined intervals.

- Portfolios are rebalanced to bring risk back in line with intended levels.

- Decisions are driven by predefined rules, not headlines or emotions.

This enforces discipline during both market rallies and drawdowns, when behavioral mistakes are most common.

3) Risk controls and defined review frequency

Risk management is embedded into the portfolio structure.

- Allocation ranges are defined in advance to prevent unintended concentration.

- Reviews follow a consistent cadence rather than ad-hoc intervention.

- Changes are made only when portfolio structure, not market noise, warrants action.

This reduces decision fatigue and ensures consistency over long investment horizons.

4) SIP and lump sum investing

Paasa supports both SIP and lump sum investing within the same framework.

- SIPs reduce the pressure of timing entry points and encourage disciplined capital deployment.

- Lump sums are allocated based on strategic allocation rather than short-term market views.

- The focus remains on long-term structure, not immediate market direction.

In both cases, the objective is to ensure capital is aligned to portfolio design from the outset.

Why UCITS ETFs fit into Paasa’s framework

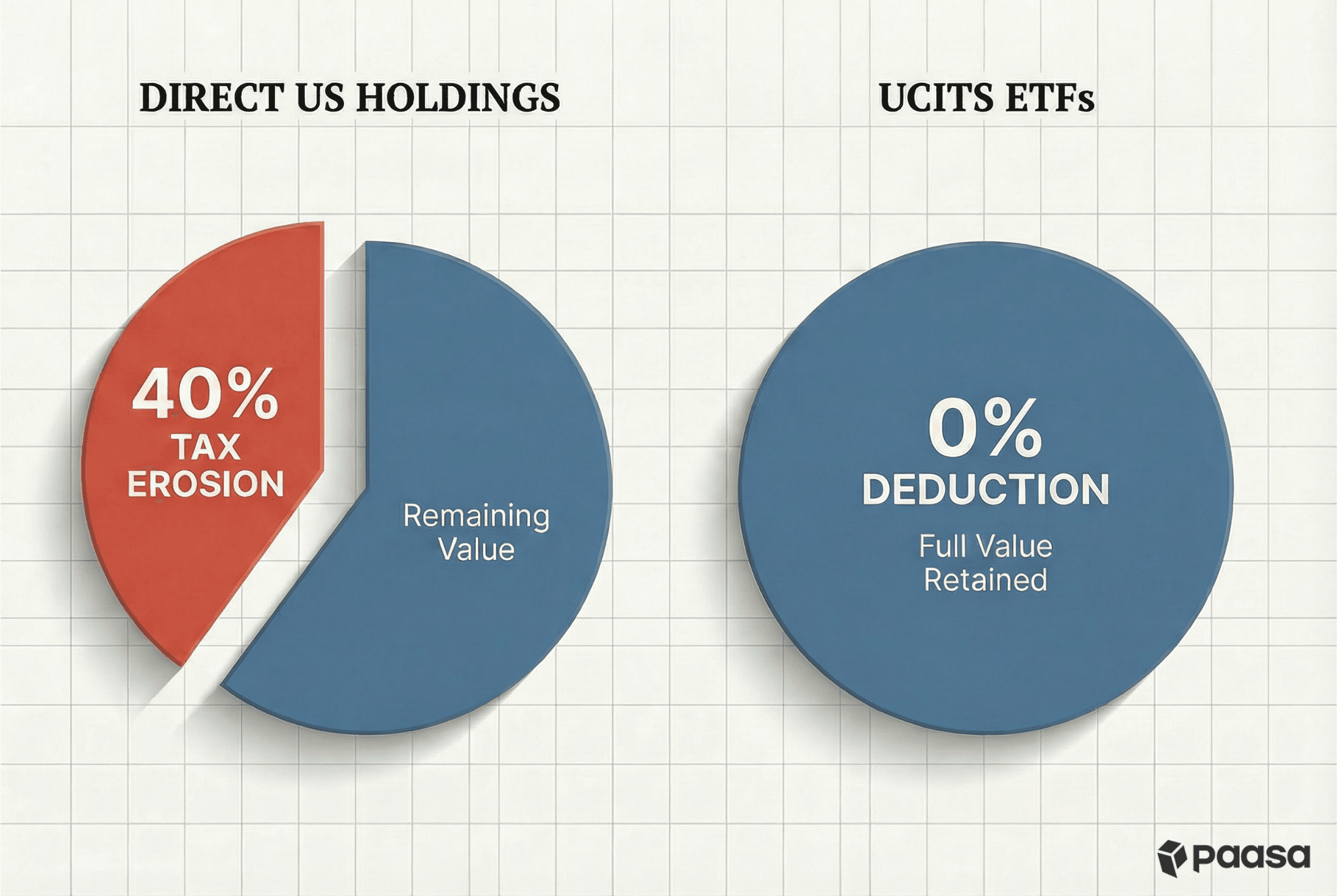

At a portfolio level, UCITS ETFs provide broad, diversified market exposure similar to US-listed ETFs.

They allow investors to participate in global equity and bond markets efficiently, with low costs and transparent construction, making them well suited for passive, long-term allocation.

Where UCITS ETFs differ is in their structure.

For Indian residents, US-listed ETFs introduce an additional layer of risk in the form of US estate tax exposure. In the event of death, US-situs assets above USD 60,000 can be subject to estate tax of up to 40%, creating a risk that is entirely unrelated to market performance or investment quality.

UCITS ETFs mitigate this risk by design. Being domiciled outside the US, they remove US estate tax exposure while maintaining comparable market participation.

UCITS ETFs are also better aligned with long-term portfolio construction from a tax and compliance standpoint.

At Paasa, UCITS ETFs are therefore not treated as a workaround or an alternative. They are a structurally better tool for implementing global, passive portfolios for Indian investors, fully aligned with the principles of Modern Portfolio Theory.

Why global investing looks different for Indian investors

Global portfolio frameworks must account for local realities.

For Indian investors, this includes:

- Currency exposure between INR and foreign assets

- Cross-border tax drag and reporting complexity

- US estate tax risk

- FEMA and LRS compliance constraints

A portfolio that works in theory but ignores these factors is structurally incomplete.

At Paasa, global frameworks are adapted for Indian investors so that outcomes remain resilient, compliant, and aligned with long-term ownership.

What Paasa deliberately does not do

Discipline requires boundaries. Paasa does not:

- Pick individual stocks

- Time markets

- Make tactical or headline-driven calls

- Chase recent performance

These are not limitations. They are safeguards designed to reduce fragility and reliance on outcomes that are difficult to repeat consistently.

What success looks like in a Paasa portfolio

Paasa is not designed to maximise returns in any single year. The objective is to deliver stable, benchmark-aligned USD outcomes over full market cycles, while controlling risk and avoiding structural vulnerabilities that can undermine long-term wealth.

This approach is suited for investors who view global investing as a long-term allocation decision and value structure, predictability, and discipline alongside growth.

Markets will change. Products will evolve. The principles behind portfolio construction should not.

That belief is the foundation on which Paasa is built.