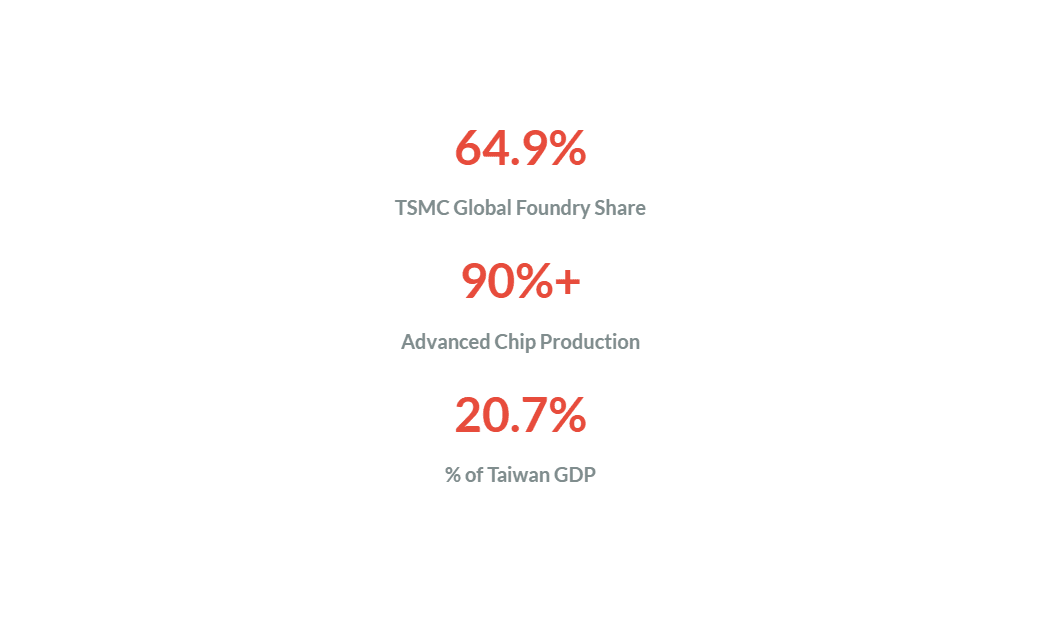

TSMC controls 64.9% of the global foundry market as of Q3 2024, up from 62.3% the prior quarter. The company's dominance is not just about market share, it is about irreplaceability. Over 90% of the world's most advanced chips, the sub 7nm nodes powering AI accelerators, smartphones, and autonomous systems, come from Taiwan. Apple, Nvidia, AMD, Qualcomm, and Broadcom all depend on TSMC's manufacturing capabilities.

There is no near term substitute.

Table of contents

Pricing the Unthinkable

The probability of a Taiwan crisis in 2026 is low but non zero. U.S. intelligence assessments recently backed away from the "2027 Davidson window," stating that China has no set timeline and prefers peaceful unification.

Analysts at Eurasia Group note that Beijing's military purges have effectively set aside invasion as an option for at least two years. Economic headwinds, slowing growth, property sector fragility, youth unemployment, compound the cost of conflict.

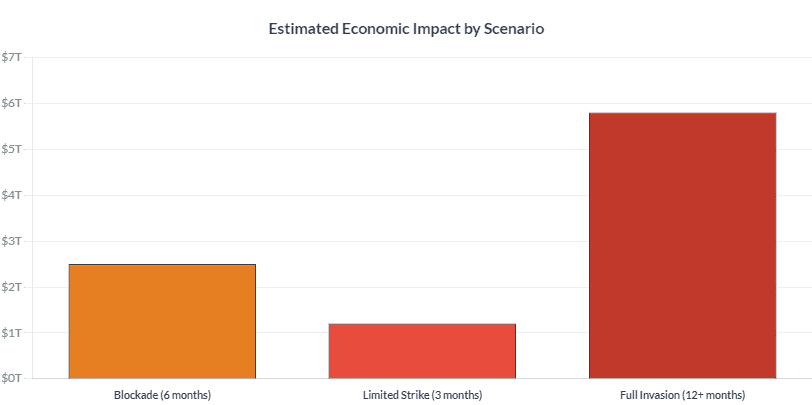

But low probability does not mean low impact. A blockade, quarantine, or precision strike scenario would immediately sever the semiconductor supply chain.

Even a grey zone escalation, cyberattacks on TSMC facilities, restrictions on rare earth exports, coercive diplomacy targeting Taiwan's diplomatic partners, would inject massive uncertainty into global tech valuations. The Council on Foreign Relations now ranks a cross strait crisis as a Tier I contingency with greater than 50% likelihood of occurring within 12 months and high impact on U.S. interests.

Markets price risk through implied volatility, credit spreads, and options skew. Taiwan exposed equities currently trade with minimal geopolitical premium.

The TAIEX (Taiwan Stock Exchange Weighted Index) has rebounded strongly from pandemic lows, with TSMC itself commanding a market cap near $1.9 trillion. Investors are either pricing the risk at zero or assuming U.S. intervention guarantees the status quo. Both are dangerous assumptions.

What a Crisis Would Look Like

Unlike the Russia Ukraine conflict, which markets largely contained as a European energy and grain shock, a Taiwan crisis would cascade globally. Three transmission channels matter:

Supply Chain Paralysis

High performance computing, already 52% of TSMC's wafer revenue, relies on continuous fab operation. A shutdown lasting even weeks would exhaust inventories. Automakers, data centers, consumer electronics, and defense contractors would face simultaneous shortages. The 2021 chip shortage, caused by pandemic related demand mismatches, cost the global economy an estimated $500 billion. A Taiwan crisis would be an order of magnitude worse.

Financial Contagion

Taiwan represents 27% of the MSCI Emerging Markets Index and 8 to 12% of many global equity portfolios through direct and indirect exposure. A sharp drawdown in TSMC and related semiconductor equities would trigger margin calls, ETF redemptions, and systematic deleveraging. Volatility would spike across all risk assets as correlations converge toward one, the hallmark of a true tail event.

Geopolitical Escalation

Japan has publicly committed to Taiwan's defense, with recent acquisitions of Tomahawk cruise missiles and anti ship weapons explicitly designed to target Chinese invasion forces. South Korea, the Philippines, and Australia would face pressure to choose sides. Unlike previous regional crises, this one carries the risk of direct U.S. China military confrontation, potentially involving nuclear armed powers.

Geographic Rebalancing

Diversification alone will not save you in a Taiwan crisis. Correlations surge to 0.9 plus during systemic shocks. But pre positioning matters. Bridgewater's research on geographic diversification highlights Japan, India, and Brazil as offering the lowest correlation to U.S. conditions.

Japan is particularly attractive: third largest bond market, fourth largest equity market, domestically focused companies, and decoupled monetary policy.

For emerging market exposure, consider ex China/Taiwan funds. The iShares MSCI Emerging Markets ex China ETF (EMXC) returned 8.5% in 2023 vs. 6.7% for the broad MSCI EM index, outperformance driven by avoiding Chinese regulatory risk and Taiwan concentration.

Freedom 100 EM ETF (FRDM) screens for economic freedom metrics, excluding authoritarian regimes entirely. These funds sacrifice some upside during risk on rallies but provide structural resilience.

Rebalancing away from Taiwan does not mean abandoning semiconductors.

U.S. listed peers like Intel, GlobalFoundries, and emerging fabs in Japan and Germany offer exposure to the secular trend without the geopolitical binary. TSMC's Arizona and Kumamoto facilities represent nearshoring efforts, though leading edge R&D remains island centric. Diversification here is about reducing single point failure risk, not exiting the sector.

Limits of Hedging

No strategy offers perfect protection. VIX options suffer contango decay and can fail in slow grinding selloffs. Gold underperformed during 2022's inflation surge as real yields rose. Geographic diversification collapses during synchronized global recessions.

The Taiwan scenario is especially challenging because it combines supply shock, financial panic, and geopolitical escalation, stressing multiple asset classes simultaneously.

Tail hedges should be sized to preserve optionality, not eliminate loss. A properly constructed program might allocate 15 to 25% of portfolio value across gold, volatility instruments, and out of the money options. This will not prevent drawdowns, but it generates liquidity when assets are crashing, enabling rebalancing at depressed valuations, the true value of crisis alpha.

Behavioral discipline matters more than precision. The worst outcome is not losing money on expired puts; it is panic selling equities at the bottom because you lacked downside protection. Hedging buys emotional resilience as much as financial protection.