Every spring, a version of the same advice circulates across financial media with the confidence of received wisdom: sell your equities, move to cash, and redeploy in November when the market has historically done its heavier lifting.

The phrase "sell in May and go away" traces its origins to nineteenth century London, where wealthy merchants and brokers would decamp to the countryside after May, leaving trading floors thin and markets sluggish until autumn. In that context, the advice made practical sense. In 2026, it borders on wealth destruction.

The mechanics of the trade sound intuitive enough. Since 1950, the S&P 500 has returned roughly 7% annualized during the November to April window versus about 2.1% from May through October.

The winter half beats the summer half, and the gap is real.

But the conclusion that investors should therefore abandon equities entirely is where the strategy collapses; because positive is still positive, and the cost of being wrong even once is compounded asymmetrically across decades.

Table of contents

- The Compounding Penalty

- The Invisible Tax of Missing Best Days

- The 2026 Specific Case Against Selling

- What Accumulation Actually Means

- Limits of This View

The Compounding Penalty

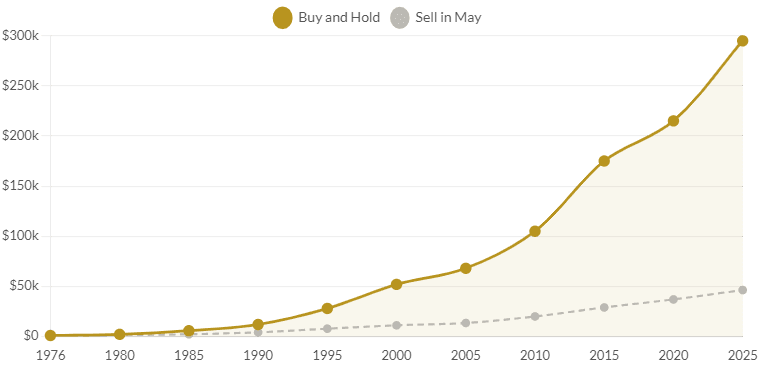

Source: American Century Investments, Bloomberg.

The magnitude of the divergence is arresting when laid out in full. An investor who placed $1,000 into the S&P 500 at the start of 1976 and never touched it would have arrived at year end 2025 with roughly $294,795.

The investor who diligently exited every April and returned every November would have accumulated just $46,351 over the same span.

That is not a modest drag. It is a six to one wealth gap manufactured entirely by calendar discipline that never needed to exist.

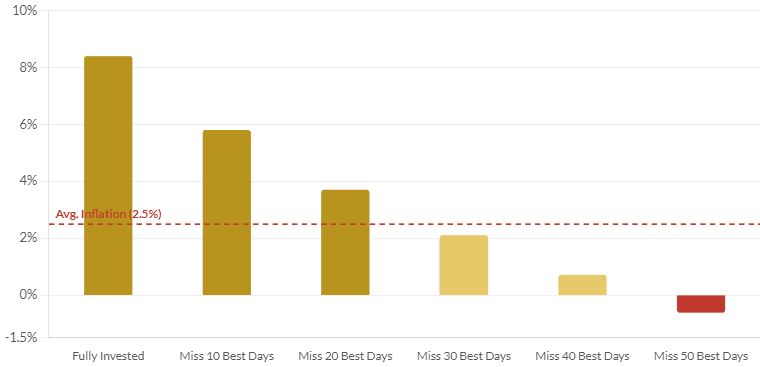

The Invisible Tax of Missing Best Days

Seasonal timing arguments obscure a more fundamental problem: the market's largest single day gains are distributed unpredictably, and they cluster disproportionately around periods of maximum fear and uncertainty.

Wells Fargo Investment Institute data covering the thirty years to June 2025 makes the arithmetic plain. A fully invested S&P 500 portfolio compounded at 8.4% per year. Miss the thirty best trading days across that entire period, roughly one day per year, and the return collapses to 2.1%, below the 2.5% average inflation rate over the same window.

The investor who thought they were managing risk was in fact running a portfolio that quietly lost purchasing power.

Franklin Templeton's parallel analysis of the twenty years from January 2005 to December 2024 is equally instructive. Across 5,033 trading days, a $10,000 investment held in full compounded at 10.35% annually.

Missing only 10 of those days, a fraction of a percent of the total, cut the return by 63%. The asymmetry exists because recovery rallies from drawdowns are violent and brief. The investor who sold in May 2020 missed a 39% surge from late May through October that year. The one who sold in May 2009 missed the opening legs of the longest bull market in modern history.

The 2026 Specific Case Against Selling

If the long run data argues against seasonal exit, the 2026 macro environment provides the contemporary punctuation.

SPY closed mid April near all time highs with the VIX in the mid teens. Roughly 78% of S&P 500 companies reporting in the first quarter beat consensus earnings estimates, above the ten year average of 74%. Semiconductors, energy, defense, and industrials are driving margin expansion.

That combination of low volatility, elevated earnings beat rates, and broad sector participation is the opposite of the conditions that have historically made summer exits pay off which tend to cluster around elevated uncertainty, stretched valuations, and deteriorating momentum.

What Accumulation Actually Means

The alternative to seasonal exit is not passive indifference to valuation. It is the deliberate use of summer softness, when it arrives as a structural entry point rather than a reason to leave.

If the May to October window delivers below average returns two thirds of the time, the investor who remains deployed still competes. In the one third of summers that disappoint materially, the disciplined accumulator with dry powder available redirects new capital rather than rotting in money market funds. The two behaviors are not identical.

In 2026, the case for accumulation centers on three sectors that have been doing the compounding work.

Semiconductors remain the physical substrate of the AI infrastructure buildout, with NVDA and AVGO leading a margin expansion cycle that has a multi-year runway as data center demand continues outrunning supply.

Energy has benefited from supply constraints and geopolitical volatility around key chokepoints.

Defense primes like LMT carry backlogs stretching beyond 24 months, giving their earnings models unusual forward visibility for a cyclical sector.

Each of these represents a theme that plays through autumn regardless of whether British aristocrats once preferred the countryside in August.

Limits of This View

Seasonal patterns do contain a kernel of structural truth.

The November to April window has historically outperformed the summer window, and the gap is statistically significant across global markets in the Bouman and Jacobsen dataset.

For investors with very short time horizons, no tax advantaged accounts, and a genuine need to deploy capital elsewhere over the summer, perhaps in private markets or real estate, the decision to trim equity exposure in May is not categorically wrong. The argument here is against treating it as a rule rather than a consideration.

Similarly, in genuine bear markets, 2022 being the most recent example, the seasonal strategy did outperform for the year. If the macro deteriorates sharply in May or June on the back of an earnings revision cycle or a geopolitical escalation that markets have not priced, the framework would look prescient in hindsight.

This piece makes no forecast about what the next six months will deliver. It argues that the decision to exit or accumulate should be made on valuations, earnings, and risk appetite and not the calendar.