The setup for the rotation was built over the first half of the year. The Philadelphia Semiconductor Index surged 83% year to date, while a separate Morgan Stanley reading put the year to date gain closer to 85%, as AI data center demand and a memory chip shortage drove pricing power for suppliers.

Over the same stretch, Bloomberg's gauge for the Magnificent Seven lost 1.9% in the first half of 2026, compared with a 9.3% gain in the S&P 500, marking one of the weakest starts to a year for the group relative to the broader market on record.

The divergence was not gentle. The Magnificent Seven collectively lost more than $2.2 trillion in market value in June as investors questioned whether hyperscaler AI spending would ever generate an adequate return, even as a single trading day sell off in the semiconductor sector in early June wiped out more than $1.4 trillion in market value, with Nvidia alone losing nearly $330 billion that day.

Trading volume told the same story: semiconductor ETFs were changing hands at more than $40 billion a day, up from roughly $9 billion a year earlier, and the sector had approached about 18% of the S&P 500, historically rare territory.

Table of contents

- The reversal, in numbers

- Why valuation is doing the heavy lifting

- What the hyperscalers are still spending

- Limits of this analysis

The reversal, in numbers

Over the past two weeks, top tier Wall Street institutions including Morgan Stanley and Goldman Sachs have called for a strategic pivot, arguing semiconductor stocks are severely overbought and advising clients to sell chips and rotate back into the Magnificent Seven.

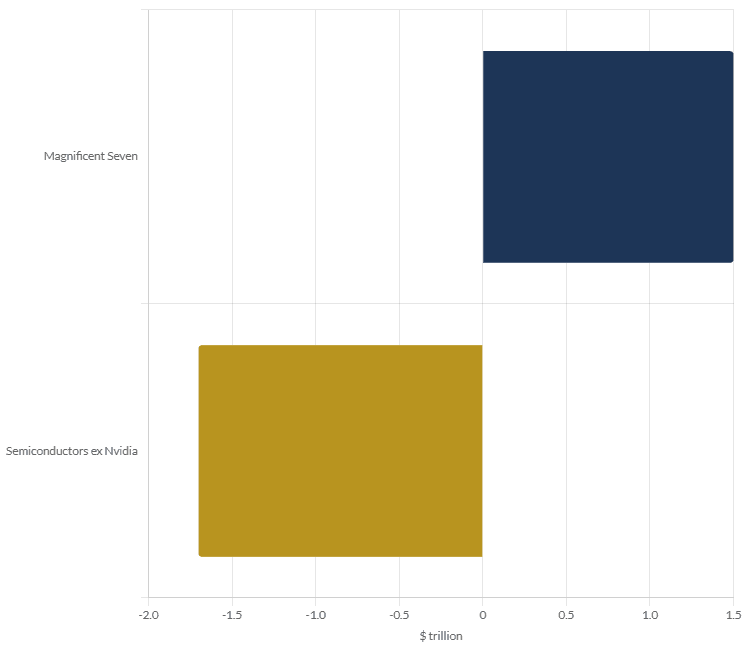

The trade has moved fast. The Magnificent Seven have added about $1.5 trillion in market value in July, while semiconductor stocks excluding Nvidia have erased nearly $1.7 trillion, a combined swing large enough that the two moves have mostly cancelled out at the index level, leaving the S&P 500 range bound for more than two months.

The breadth of the move extends beyond a handful of headline names.

Forty four of 51 software stocks in one industry basket were positive in July with a median gain of roughly 6%, while only a handful of 62 semiconductor stocks were higher and the median chip stock was down nearly 20%.

A single session captured the mood shift well: on July 16, Dell dropped nearly 10% and Micron, Western Digital, SanDisk and SK Hynix each fell about 8%, while the Magnificent Seven index rose 2.47%, with Apple climbing about 4% to a new all time high and Alphabet, Microsoft, Meta and Amazon each up roughly 3%.

Why valuation is doing the heavy lifting

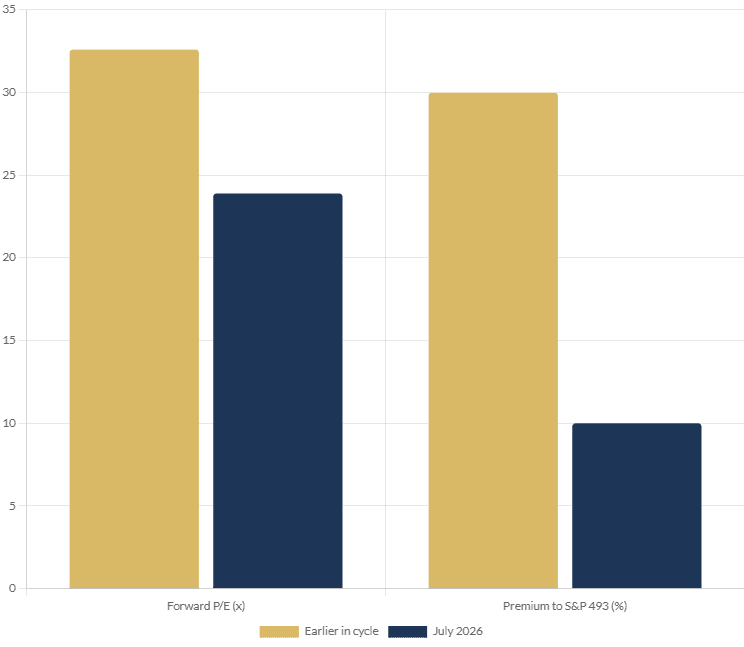

The rotation is as much a valuation story as a momentum one. The Magnificent Seven's overall price to earnings ratio has fallen from 32.6 times to 23.9 times, with its valuation premium nearing a historical low, even though the group still carries a 45% annual earnings growth advantage.

Morgan Stanley frames the gap in relative terms: the price to earnings premium the Magnificent Seven commands over the other 493 S&P 500 companies has held above 30% for most of the 2020s but is now closer to 10%, the smallest premium in more than a decade.

Not every member of the group has struggled equally. Six of the seven Magnificent Seven names have lagged the S&P 500 in 2026, with Alphabet the sole outperformer, up 14.5% year to date versus roughly 9% for the benchmark.

Nvidia sits in an unusual middle position: the stock now trades at approximately 18 times forward earnings, well below its long term historical average of 36 times, even as it has still risen 9.5% in 2026, roughly in line with the broader market after an extraordinary multi year run.

What the hyperscalers are still spending

The rotation back into mega cap tech is not a bet that AI spending slows. AI infrastructure spending among Big Tech firms is set to surpass $700 billion in 2026, a 70% year over year increase, and Amazon, Alphabet, Meta and Microsoft alone are on track to spend as much as $725 billion on capital expenditure this year.

The argument from firms like Morgan Stanley is not that the build out is ending but that the market had mispriced who captures the economics of it, favoring suppliers over the platforms that ultimately monetize the infrastructure.

That framing has produced some cautious optimism on the sell side. One Goldman Sachs strategist has pointed to the group beating earnings expectations by 13% even as prices fell, arguing the disconnect leaves valuations more reasonable, while noting many mutual and hedge funds remain underweight the group, leaving room for institutional buying if sentiment continues to improve. Price targets have followed the mood:

Bank of America has set a $350 price target on Nvidia, implying nearly 80% upside from current levels.

The move away from semiconductors and toward the Magnificent Seven over the past month is a valuation unwind, not a retreat from the AI theme itself.

Hyperscaler capital spending is still rising toward $700 billion plus in 2026, and Wall Street's argument is that the platforms doing that spending, not only the suppliers selling into it, are now the cheaper way to own the build out.

For investors, the practical read is that concentration risk has simply changed shape rather than disappeared. The Magnificent Seven still represent roughly a third of the S&P 500, and a further snapback in either direction, chips reasserting themselves or mega cap tech overshooting on the rotation, would move the whole index.

Limits of this analysis

Market cap and valuation figures cited here are drawn from a mix of Bloomberg, Morgan Stanley, and financial media reporting over a fast moving two to four week window, and some source figures diverge slightly, for example on the exact year to date gain in the Philadelphia Semiconductor Index.

Earnings season for both hyperscalers and chipmakers is still ahead in the coming weeks and could reverse or accelerate the rotation described here. This piece describes a market narrative and reported positioning shift; it is not a recommendation to buy or sell any security.