No major equity index in the world has moved like the KOSPI in 2026. From a 52-week low of 2,877, the benchmark surged to an intraday peak of 8,933 on June 2, a run that left global index trackers scrambling for comparisons.

At the index's peak, the year-to-date gain had crossed 100 percent, putting it in company with hyperinflationary outliers, not peer-group mature markets.

Goldman Sachs raised its 12-month target to 12,000 in early June, implying a further 35 percent from current levels, citing projected earnings growth that remains strong even after the index's dramatic rerating.

That is not a contrarian call; it reflects a consensus view that the earnings cycle underpinning Korean equities has years of runway left.

The engine behind all of it is narrow but powerful. Samsung Electronics and SK Hynix together account for roughly half the index's total market capitalisation, and both are first-order beneficiaries of the global AI infrastructure buildout.

When hyperscalers accelerate data centre spending, the first hardware constraint they hit is high-bandwidth memory. South Korea makes most of the world's supply.

Table of contents

- Performance Comparison

- The Memory Cycle and Why It Has Legs

- The Korea Discount and Why It May Finally Be Closing

- The MSCI Question: A Catalyst Deferred & Cancelled

- What to Watch: The Forward Catalyst Map

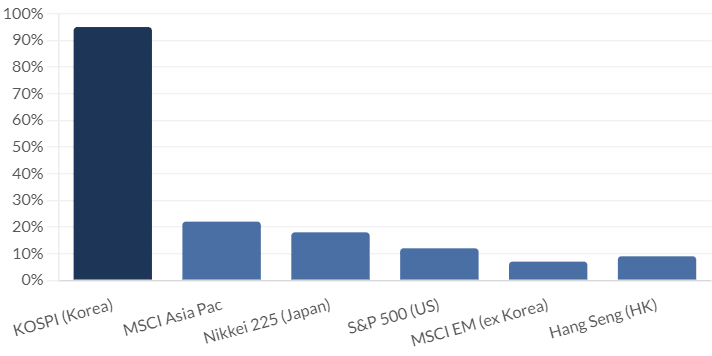

Performance Comparison

The breadth picture is, however, striking in its narrowness.

Jonathan Krinsky, chief market technician at BTIG, noted that over six consecutive sessions in which the KOSPI gained 12 percent, breadth was negative on every single day, and not marginally so. The entire move was engineered by a handful of names. That concentration creates an index that functions less like a broad equity market and more like a leveraged call option on global AI capex sentiment.

Every Fed communication, every hyperscaler earnings call, every geopolitical development touching technology supply chains lands on the KOSPI with amplified force.

Volatility Profile

The Memory Cycle and Why It Has Legs

The fundamental driver of the KOSPI rally is straightforward: South Korea has a near duopoly on high-bandwidth memory (HBM), the single most constrained component in AI accelerator design.

HBM chips stack multiple DRAM dies vertically and connect them through thousands of microscopic channels, enabling the data throughput that large language model inference demands. Samsung and SK Hynix are the only two producers at meaningful scale. Nvidia cannot ship its H100 or B200 without their output. That structural position has turned both companies into royalty-collecting infrastructure plays on every dollar of hyperscaler AI spending.

In a telling milestone that went largely unreported outside Korea, SK Hynix overtook Samsung Electronics as the country's most valuable listed company during the rally, reflecting the market's judgment that its HBM execution has been superior. Samsung reported HBM4 sales exceeding one billion dollars within four months of the product's commercial launch, a ramp rate that has surprised even bullish analysts.

Micron's June 2026 earnings confirmed that AI-driven demand is accelerating, not plateauing. Micron's upbeat revenue outlook functioned as a third-party validation of the thesis that the memory supercycle is still in early innings.

The Korea Discount and Why It May Finally Be Closing

For decades, Korean equities traded at a structural discount to comparable markets. The average price-to-book ratio of the KOSPI hovered around 0.99, well below advanced and emerging market peers despite the presence of world-class industrial and semiconductor champions.

More than 60 percent of listed Korean firms recorded a return on equity below the long-run average of 7 percent. The root causes were well understood: chaebol-dominated ownership structures, opaque management, weak minority shareholder protections, and capital allocation practices that served controlling families at the expense of outside investors.

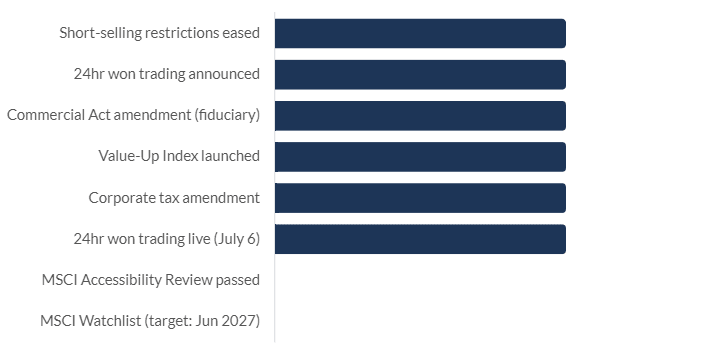

The government's Corporate Value-Up Programme, launched formally in 2024 and given legal force through Commercial Act amendments in 2025, represents the most substantive governance reform in the country's post-war history. Directors must now balance corporate interests with equitable treatment of all shareholders, not just majority owners.

In February 2026, the government tightened the framework further, amending corporate tax law to require high-dividend companies to disclose Value-Up plans to maintain their preferential tax treatment.

Banking sector payout ratios are projected by J.P. Morgan to improve from 36 percent in 2023 to above 50 percent by end-2026. The Korea Value-Up Index, which tracks companies meeting governance criteria, has outperformed the KOSPI 200 by more than 30 percent since its launch in late 2024.

The MSCI Question: A Catalyst Deferred & Cancelled

South Korea has been classified as an emerging market by MSCI since 1992, with a brief period on the developed market watchlist that ended in 2014 due to inadequate progress on foreign exchange market access. The gap between classification and economic reality has been a persistent source of the Korea Discount. An upgrade would trigger automatic portfolio rebalancing across trillions of dollars in passive and systematic strategies, with estimates of $40 to $60 billion in resulting inflows.

The June 2026 classification review produced a disappointment: MSCI kept Korea in its emerging market category. The index provider cited limited convertibility of the Korean won in offshore currency markets, a rigid investor identification system, and restrictions on in-kind transfers and off-exchange transactions.

Korea's Finance Ministry acknowledged that some reforms remained underway and that completed measures needed more time to demonstrate results. However, the crucial reform is now imminent: 24-hour trading in the dollar-won spot market is scheduled to begin on July 6, 2026. Round-the-clock foreign exchange access is the single most cited obstacle to foreign participation, and its removal, if implemented smoothly, makes watchlist inclusion at the 2027 review a live scenario.

MSCI Classification Timeline

What to Watch: The Forward Catalyst Map

Three near-term events define the range of outcomes for the KOSPI over the next six months. The first is the July 6 launch of 24-hour won trading. Smooth implementation would meaningfully improve Korea's probability of landing on the MSCI developed market watchlist in June 2027 and sustain the foreign institutional buying that has been a structural underpinning of the rally. A delayed or technically troubled rollout would set the MSCI timeline back by another year and remove a significant narrative catalyst.

The second is the July quarterly earnings season, when Samsung Electronics and SK Hynix report. With the two companies representing roughly half of index market capitalisation, their guidance on HBM pricing, order visibility, and capital expenditure plans will function as a de facto earnings release for the KOSPI itself. Any signal of demand deceleration from hyperscaler customers — which have their own earnings releases in the same window — could compress the index with the same speed it compressed in the June 23 session.

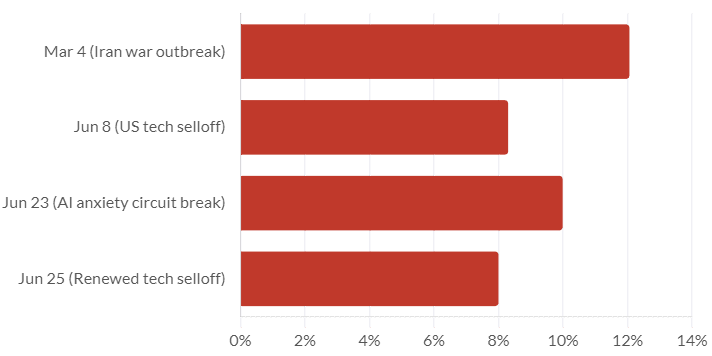

The third is geopolitical: the Iran war backdrop, specifically the stability of the Strait of Hormuz ceasefire reached in late June. The KOSPI's single largest decline of 2026 of about 12.06 percent on March 4 followed the outbreak of that conflict. Oil price spikes from renewed Hormuz disruption would feed into semiconductor manufacturing costs and suppress global risk appetite with disproportionate effect on a high-beta market like Korea. The ceasefire has eased demand for safe-haven assets and brought oil off its highs, but the agreement remains fragile by most analyst assessments.