Indian professionals who are moving back from Singapore often lack clarity about how they can manage their overseas holdings like global stocks, ETFs, and retirement accounts (CPF and SRS) after returning to India.

This article explains how you can manage your global holdings after moving back to India, and the Indian tax and reporting requirements you will be subject to.

We also cover your tax residency status, how it changes, and how you can use RNOR rules to extend the tax-free benefits you enjoyed on your capital gains in Singapore.

Table of contents

- What happens to my stocks when I move back to India?

- What happens to my CPF and SRS accounts?

- What happens to my Singapore property when I move back?

- What happens to my RSUs and stock options when I move back?

- What do I need to do with IRAS before leaving Singapore?

- Tax and reporting implications of moving back to India

- What is RNOR status and how does it affect me?

- Common Questions NRIs Have About Moving Back from Singapore

- About Paasa

What happens to my stocks when I move back to India?

Most brokerage firms used by expats in Singapore are designed primarily to serve local residents. When you move back to India, your tax residency changes, and many platforms are not equipped to handle accounts that comply with Indian tax and foreign exchange laws.

Here is how different platforms typically handle the move:

- Retail Brokerages (Tiger Brokers, Moomoo, DBS Vickers): These platforms are built heavily around Singapore residency. If you update your KYC address to India or they detect a permanent change in your tax status, they may restrict your account, pause your ability to add new funds, or in some cases, force you to liquidate your positions entirely.

- Global Brokers (Interactive Brokers Singapore, Saxo Bank): These international brokers are more flexible and usually allow you to convert your profile to an Indian resident account. However, you will likely face operational hurdles. You are left to manage complex Indian tax reporting manually (like Schedule FA), you face restrictions on certain funds, and funding the account from India going forward can incur high wire transfer fees and poor FX rates.

Note: Your capital gains from stocks and ETFs will become taxable when you become a tax resident (Resident Ordinarily Resident) in India. Consider resetting your cost basis while you are a Singapore resident or RNOR in India to reduce your final tax liability when you eventually sell these investments.

What's the best way to stay invested globally after moving back to India?

The best way to stay invested globally after moving back to India is transferring your investments into a platform that is specifically made for global investing from India.

These platforms will allow you to maintain your positions and trade as usual, while providing India-specific compliance support like filing Form W-8BEN (for investments in the US) and generating tax documents tailored for Indian reporting requirements.

What happens to my CPF and SRS accounts?

Your primary retirement savings in Singapore are fully portable. You do not have to close them when you leave, but you need to understand how India will tax them once you become a resident.

Supplementary Retirement Scheme (SRS)

This is a voluntary deferred-tax scheme. You can absolutely keep this account open after moving to India.

- Singapore Tax: If you withdraw on or after the statutory retirement age (currently 63), 50% of the withdrawal is tax-free. However, on the remaining taxable 50%, Singapore still retains taxing rights even after you move. Your bank will automatically apply a 15% or 24% withholding tax before sending the money to India. (Note: You can file a non-resident tax return with IRAS later to claim a refund if this withholding exceeds your actual tax bracket).

- India Tax: Once you are a full Indian resident, these withdrawals are taxed at your standard slab rates. To avoid double taxation, the India-Singapore DTAA allows you to take the withholding tax you paid to Singapore and use it as a "Foreign Tax Credit" to directly reduce your Indian tax bill.

When is the best time to make SRS withdrawals?

If you quality for the RNOR status, this RNOR window changes the tax cost of SRS withdrawals significantly. During RNOR, SRS withdrawals received in your Singapore bank account are not taxable in India at all. The India-Singapore DTAA credit mechanism only becomes relevant after you become a full ROR.

Central Provident Fund (CPF)

CPF is mandatory for locals and Permanent Residents, but some work visa holders (EP) may have opted in or hold legacy accounts. If you have contributed to a CPF, your Ordinary, Special, and Medisave accounts you will be able to withdraw at age 55 and beyond.

- Singapore Tax: Withdrawals from your CPF are completely tax-free in Singapore.

- India Tax: Once you become a full Indian tax resident, India treats CPF payouts as pension income. It will be taxed at your standard Indian slab rates. Singapore has primary taxing rights, but India collects the residual tax.

What happens to my Singapore property when I move back?

Singapore has no capital gains tax on property. Whether you sell your Singapore property as a resident, a non-resident, or years after leaving, Singapore does not tax the gain. The question is entirely about India.

During RNOR

If you sell your Singapore property while you hold RNOR status, the capital gain is completely exempt in India, provided the sale proceeds are received in your Singapore bank account first. You effectively pay 0% tax in both countries.

This is the most efficient window to sell if you are planning to.

After becoming ROR

Once you are a full Indian Resident (ROR), India taxes the gain as long-term capital gains at 12.5% without indexation (for property held over 24 months, under post-2024 budget rules). Since Singapore taxes nothing, there is no foreign tax credit available and India collects the full rate. Under Article 13 of the India-Singapore DTAA, gains from immovable property carry shared taxing rights between both countries. Singapore chooses not to tax, and India retains its right to tax as your country of residence.

Rental income from Singapore property

If you continue to hold Singapore property and rent it out after returning to India, the rental income treatment depends on your residency status:

- During RNOR: Rental income received in your Singapore bank account is tax-free in India. If received directly in an Indian account, it becomes taxable immediately. Read our guide on foreign rental income for RNORs for the full treatment.

- After becoming ROR: The rental income becomes taxable in India at your applicable slab rate. Singapore does not withhold tax on residential rental income paid to non-residents, so there is no foreign tax credit available and the full Indian slab rate applies.

Note: Singapore's Additional Buyer's Stamp Duty (ABSD) rules mean that non-residents face significant costs when buying additional property in Singapore. If you are already a non-resident considering selling, be aware of the ABSD implications before you buy again.

What happens to my RSUs and stock options when I move back?

Indian professionals in Singapore's tech, finance, and startup sectors commonly hold RSUs or stock options. Singapore has no capital gains tax, so RSUs that vested while you were a Singapore tax resident attracted no Singapore CGT. However, Singapore does tax RSU gains as employment income at the time of vesting, and there are specific rules that apply when you leave.

The deemed exercise rule at tax clearance

When you leave Singapore, your employer must file Form IR21 (tax clearance) with IRAS at least one month before your last day. At that point, the deemed exercise rule applies: any unvested RSUs or unexercised stock options you hold at the time of tax clearance are treated as if they vested or were exercised on that date, and Singapore income tax is assessed on the notional gain immediately.

This means you cannot leave Singapore with unvested RSUs and defer the Singapore tax until they actually vest. IRAS taxes them upfront at clearance, based on the market value on the deemed exercise date.

What this means practically

If you have significant unvested RSUs at the time of departure, Singapore will assess income tax on the full notional gain at your marginal rate. Your employer will withhold this from your final salary and any other monies owed to you. If the amounts withheld are insufficient to cover the tax, you are required to make up the shortfall before you leave.

India tax treatment after return

RSU shares you already hold at the time of return (having already been taxed in Singapore at vesting or under the deemed exercise rule) are simply foreign assets. If you sell them during RNOR, the capital gain is tax-free in India. If you sell after becoming ROR, the gain is taxable in India as foreign capital gains, and you can claim a foreign tax credit for any Singapore tax already paid.

Note: If your employer applies for the Tracking Option with IRAS as an alternative to the deemed exercise rule, the actual tax is deferred until the RSUs vest or options are exercised. This can work in your favour if you expect the share price to fall after departure. Ask your employer's equity team whether they have applied for this option.

What do I need to do with IRAS before leaving Singapore?

Unlike returning from some other countries, Singapore has a formal tax exit process that every non-citizen must complete before leaving. Missing or delaying this process can result in your final salary being withheld and penalties for your employer.

Tax clearance (Form IR21)

When you leave your Singapore employer permanently, your employer is legally required to file Form IR21 with IRAS at least one month before your last day of employment. IRAS will then assess your total Singapore tax liability and issue a Clearance Directive.

Your employer must withhold all monies owed to you, including salary, bonus, leave encashment, gratuity, and any other payments, from the date they are aware of your departure. These funds are held until IRAS issues the Clearance Directive confirming your tax has been settled.

Most IR21 forms are processed within 21 days when filed electronically. Once cleared, IRAS will either direct your employer to remit a portion to IRAS for tax owed, or release the full withheld amount to you.

What to tell your employer before you resign

Give your employer as much notice as possible, specifically to allow them time to file IR21 before your last day. If your employer files IR21 late, they face a fine of up to SGD 5,000 per offence. As a result, most HR teams in Singapore are familiar with this process, but it is still your responsibility to flag it early.

If you have SRS contributions or withdrawals

If you have an SRS account and make a withdrawal at tax clearance, that withdrawal is treated as a premature withdrawal and the full amount (not just 50%) is taxable, with a 5% penalty. If you plan to withdraw your SRS balance, it is generally more efficient to wait until you have reached the required age (64 from July 1, 2026) and do so in a structured way over multiple years during your RNOR window. Discuss the timing with your SRS bank operator before submitting your resignation.

Note: You must settle all Singapore tax before you leave. IRAS will not issue your Clearance Directive until your tax liability is paid in full. If your withheld monies are insufficient to cover the tax assessed, you will receive a Statement of Account requiring you to pay the shortfall within 7 days.

Tax and reporting implications of moving back to India

When you permanently return to India from Singapore, your tax status eventually shifts from being a Non-Resident Indian (NRI) to a Resident.

This brings two major changes: your global income becomes taxable in India, and your reporting requirements increase significantly.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How Global Stocks and ETFs Are Taxed for Indian Investors

- Tax on Repatriation of Foreign Income to India

- Foreign Asset Disclosure (Schedule FA) Requirements for Indians

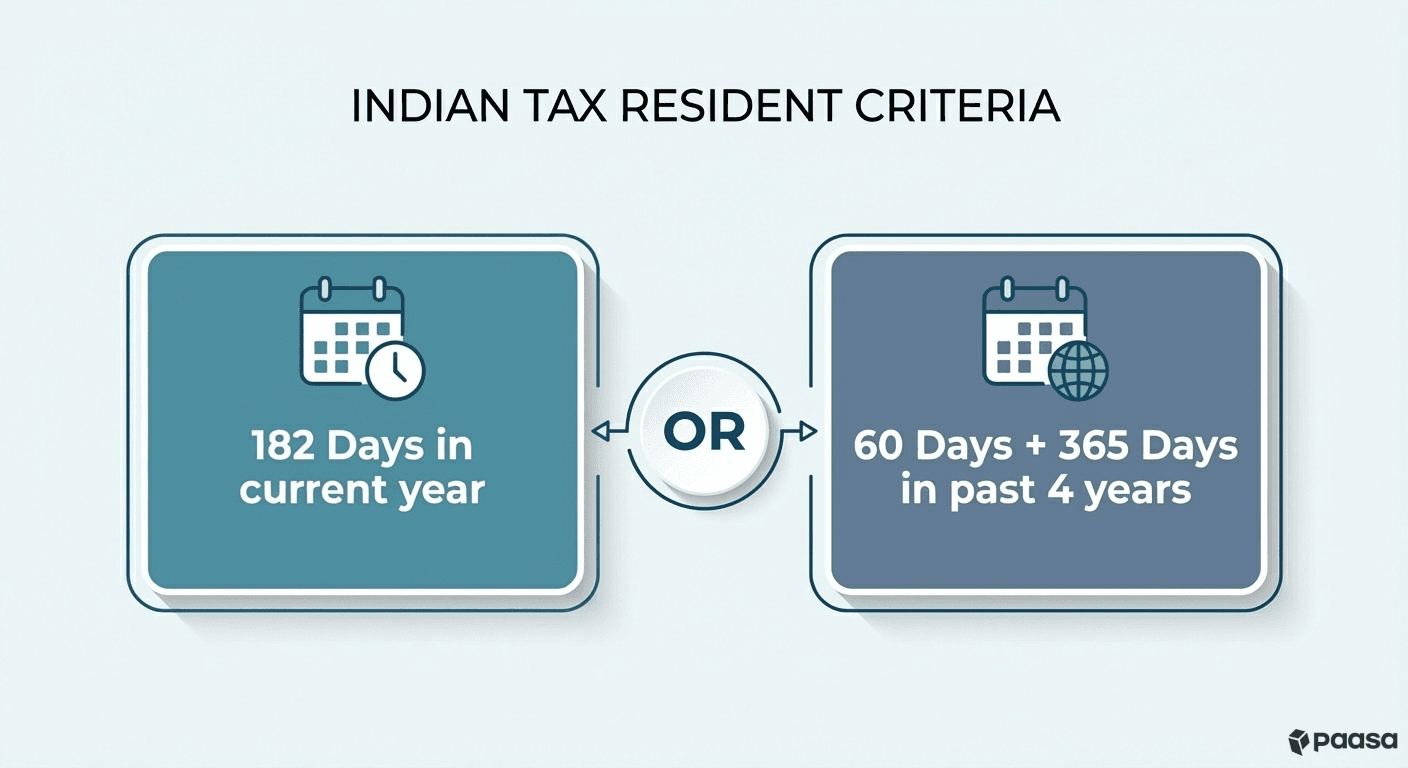

When do you become an Indian Tax Resident?

Under the Income Tax Act, you are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in the four preceding tax years (60-day rule).

Once you meet this criterion, you are legally required to pay tax in India on income earned anywhere in the world.

What is RNOR status and how does it affect me?

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status that makes your global income tax-free for a few years even after you become a tax resident in India.

It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You typically qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

This status grants you a 1 to 3-year window where your global income is treated differently from that of a standard Indian resident.

What benefits can I get from this status?

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your overseas assets without immediate tax liability.

- Global Stocks & ETFs: If you sell them while you are RNOR, the capital gains are completely tax-free in India. Since Singapore does not levy capital gains tax either, you effectively pay 0% tax. You can use your RNOR window to sell your stocks, reset your cost basis, and reinvest without a tax penalty.

- Foreign Bank Interest: The interest earned in your Singapore or offshore bank accounts remains tax-free in India.

- Dividends: Dividends earned from global stocks remain tax-free in India during this period.

To utilize these exemptions, you must receive the funds in your foreign bank account first. If you wire sale proceeds or dividends directly to an Indian bank account, the income is considered "received in India" and becomes fully taxable immediately.

Common Questions NRIs Have About Moving Back from Singapore

Can I send money from India to fund my global investments?

Yes. You can remit up to $250,000 USD equivalent per financial year under the Liberalised Remittance Scheme (LRS) to invest in foreign stocks or ETFs.

However, be aware that transfers exceeding ₹10 Lakhs in a year attract a 20% TCS (Tax Collected at Source). This is an advance tax that you can claim back as a refund or adjust against your tax liability when filing your income tax return in India.

To learn more about how you can send money abroad while complying with Indian regulations, read our Complete LRS Guide for Indians.

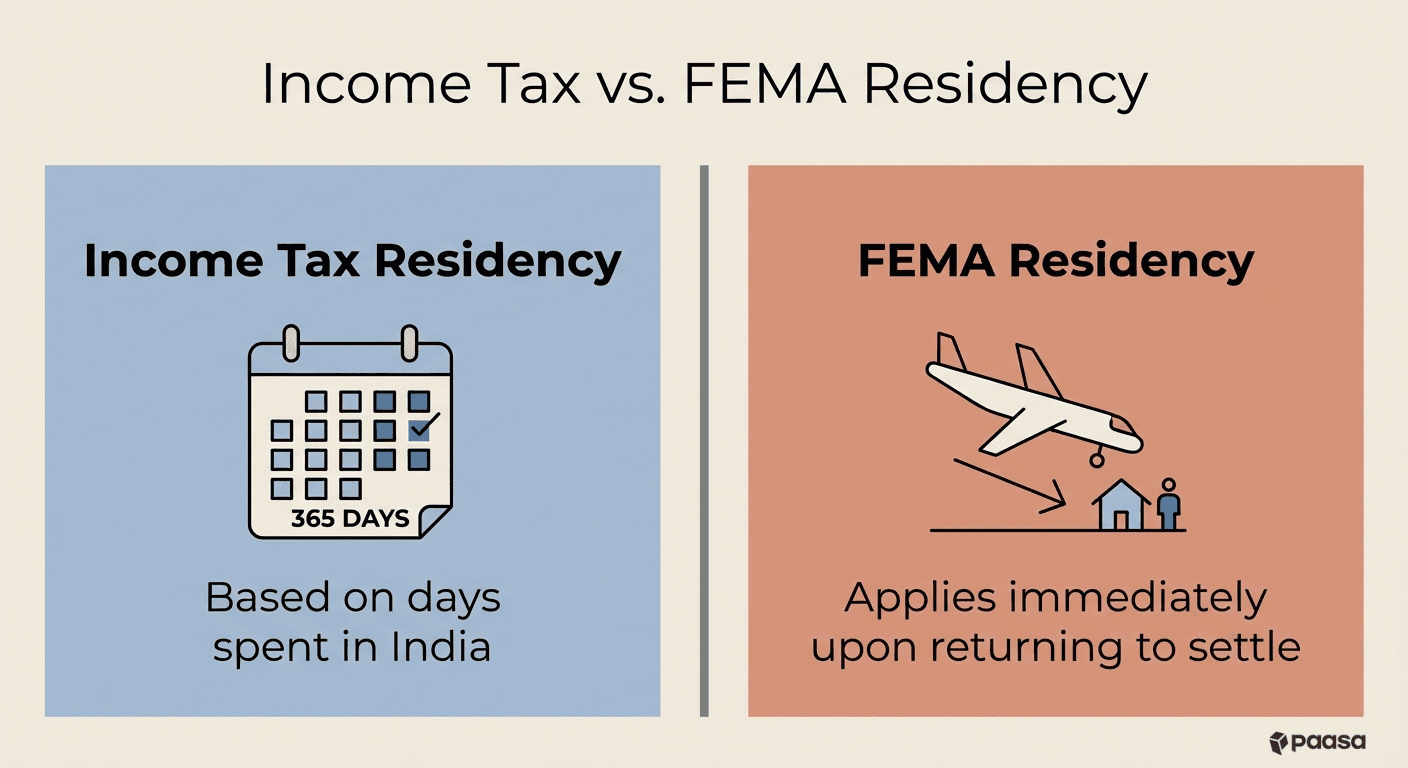

When do I become subject to FEMA upon moving back?

You become a resident under the Foreign Exchange Management Act (FEMA) immediately upon landing in India if your intention is to stay for an uncertain period or for employment and business.

Unlike income tax residency (which counts the number of days you stay), FEMA residency applies the moment you return to settle.

Can I continue operating my Singapore bank account?

Yes. Section 6(4) of FEMA allows you to continue holding and operating foreign bank accounts, overseas stocks, and properties if they were acquired when you were a resident outside India. You are not legally required by the Indian government to close your DBS, OCBC, or UOB bank accounts.

Can I keep my NRO account?

No. Once your status changes to Resident, you are legally required to inform your bank and convert your NRO and NRE accounts to a standard Resident Savings Account. Continuing to hold an NRO or NRE account as a resident is a violation of FEMA regulations.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore, and we support 9 global currencies.

- Seamless In-Kind Transfers: You can move your entire global stock portfolio (from international brokers like Interactive Brokers Singapore or Saxo) directly to Paasa. This allows you to consolidate your assets in one place without selling them and triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures. We eliminate the need for manual calculations for Schedule FA and capital gains.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents holding US-domiciled assets.